Understanding Your Credit Score

Good Credit Score: How to Achieve It?

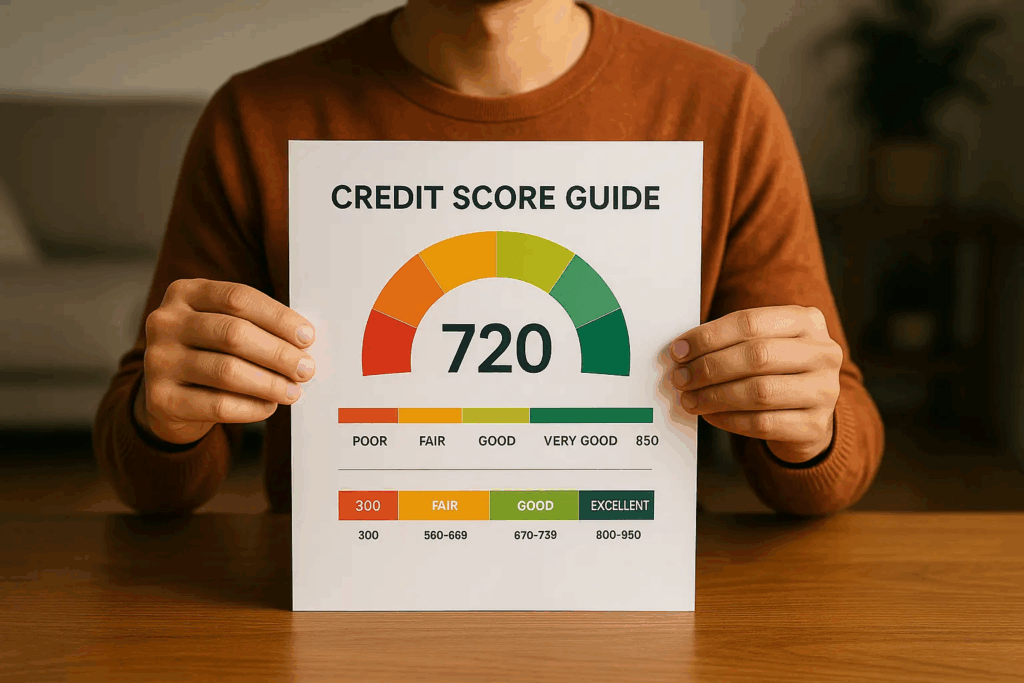

A credit score (300–850) reflects your current financial management—not your personal worth. In 2023, the average American score was 715. A score above 670 (FICO®) or above 661 (VantageScore®) generally unlocks competitive rates for loans, housing, or even insurance. The biggest influences on your score are on-time payments (35%), your credit utilization ratio (30%), and length of account history (15%). Fixing errors can save you up to $50,000 on a home loan, based on average rates. Improve your score for free via AnnualCreditReport.com, avoid closing old accounts, and lower your credit utilization. Understanding how these factors work helps you take control—without falling for false promises.